The Ministry of Justice corrected a large part of its accounting errors; however, some figures in the 2020 annual accounts are unreliable

Press Release on audit No 20/25 – 15 November 2021

The Supreme Audit Office examined the data of the closing account, accounting and preparation of the 2020 annual accounts of the Ministry of Justice (MoJ). The auditors also focused on the data submitted by the MoJ for the assessment of the implementation of the state budget. The closing account and the data submitted for the assessment of the implementation of the 2020 state budget were free from material misstatements. However, some figures in the 2020 annual accounts are unreliable.

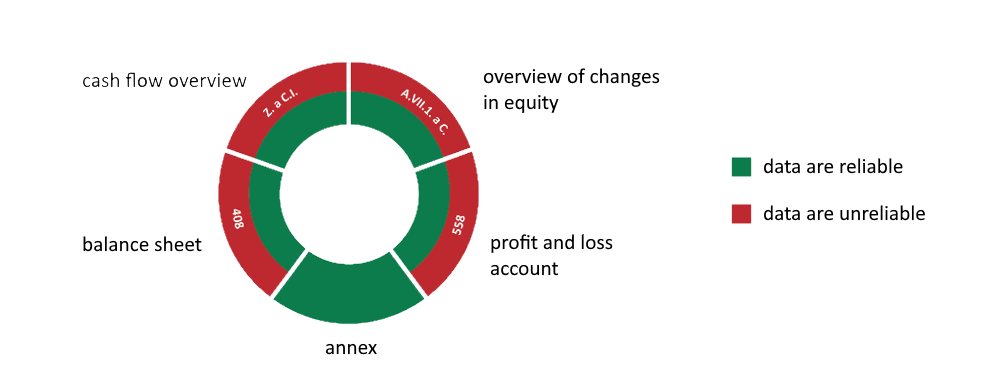

The audit was initiated before the end of the year 2020. This allowed the MoJ to correct certain accounting misstatements detected during the audit before the closure of the 2020 financial year. The MoJ then drew up its annual accounts which, however, contained further misstatements amounting to almost CZK 51 million. The MoJ also corrected these misstatements, but it also made accounting entries surpassing CZK 106 million, and by doing so it had reclassified the costs of the year 2020 under the year 2019. This resulted in a material misstatement in the new 2020 annual accounts, which was subsequently drawn up by the MoJ, therefore several statements of the annual accounts were affected. Consequently, the data on the items in question in those statements is unreliable. However, as for all the other data, the annual accounts, according to the SAO, give a true and fair view of the subject matter of the accounts.

Some system weaknesses were also identified by the auditors in the accounting. Apart from the incorrect accounting for travel costs, the weaknesses were mainly caused by the incorrect settings and the application of the accrual method for recurrent payments. This led to erroneous accounting of the costs of technical software support in the order of millions of Czech crowns.

The SAO also drew attention to weaknesses in the inventory of assets, particularly in the area of small long-term intangible assets and software. In some cases, the MoJ did not identify differences between the actual and the book values of the assets.

The auditors also examined how the MoJ had remedied the deficiencies found in the previous SAO audit. All 16 measures were fully and correctly implemented by the MoJ.

Reliability of accounts following accounting corrections

Communication Department

Supreme Audit Office